How Would You Like to Retire at 55 — for Free? More of New York's Public Workers Soon May.

The bill will go to you, the taxpayer—but not before it wrecks Mayor Mamdani’s budget

Imagine you could retire at 55. A guaranteed pension of roughly 60 percent of your salary in addition to, not instead of, Social Security, paid monthly for the rest of your life and exempt from state income tax. After 10 years on the job, you’d contribute nothing toward it from your own paycheck. It wouldn’t fluctuate with the stock market, unlike your 401(k). If the pension fund ran short, your neighbors would make up the difference.

You can’t have this—unless you were hired as a New York City teacher or municipal worker before 2009. Today, the city’s most powerful unions are fighting to restore these platinum-clad retirement benefits for every worker hired since.

They’re close to winning. The bill will go to you, the taxpayer—but not before it wrecks Mayor Mamdani’s budget.

How We Got Here

New York City has five public pension funds covering teachers, police, firefighters, and other city workers. These are defined-benefit pensions, meaning employees receive a guaranteed monthly payment in retirement (often with cost-of-living adjustments) regardless of how financial markets perform. New York’s pensions are also both state-tax exempt and constitutionally guaranteed, meaning benefits can only go up, never down, and that taxpayers must make up the difference when investments don’t deliver the expected returns.

New York’s original pension systems, created over 100 years ago, didn’t require employees to pay into them and gave full pensions at age 55. That approach ran into trouble as more people lived longer in retirement, so the state Legislature enacted reforms in the 1970s to make the funds more sustainable by creating new “tiers” of benefits for future employees. Among other things, they required workers to pay into the system and to wait until age 62 before collecting a full pension.

But state lawmakers soon began chipping away at those reforms, restoring the age 55 retirement if employees had worked 30 years. In 2000, they enacted a massive “sweetener” that allowed employees who’d been on the job at least 10 years to stop paying in.

Examining the resultant fiscal wreckage, my colleague E.J. McMahon explained:

At the time, proponents claimed these changes would not require an increase in pension contributions, as long as the rate of return on investments remained at 8 percent. But the retirement systems proceeded to lose money over the next two years—a risk that no one involved in the 2000 changes was willing to acknowledge.

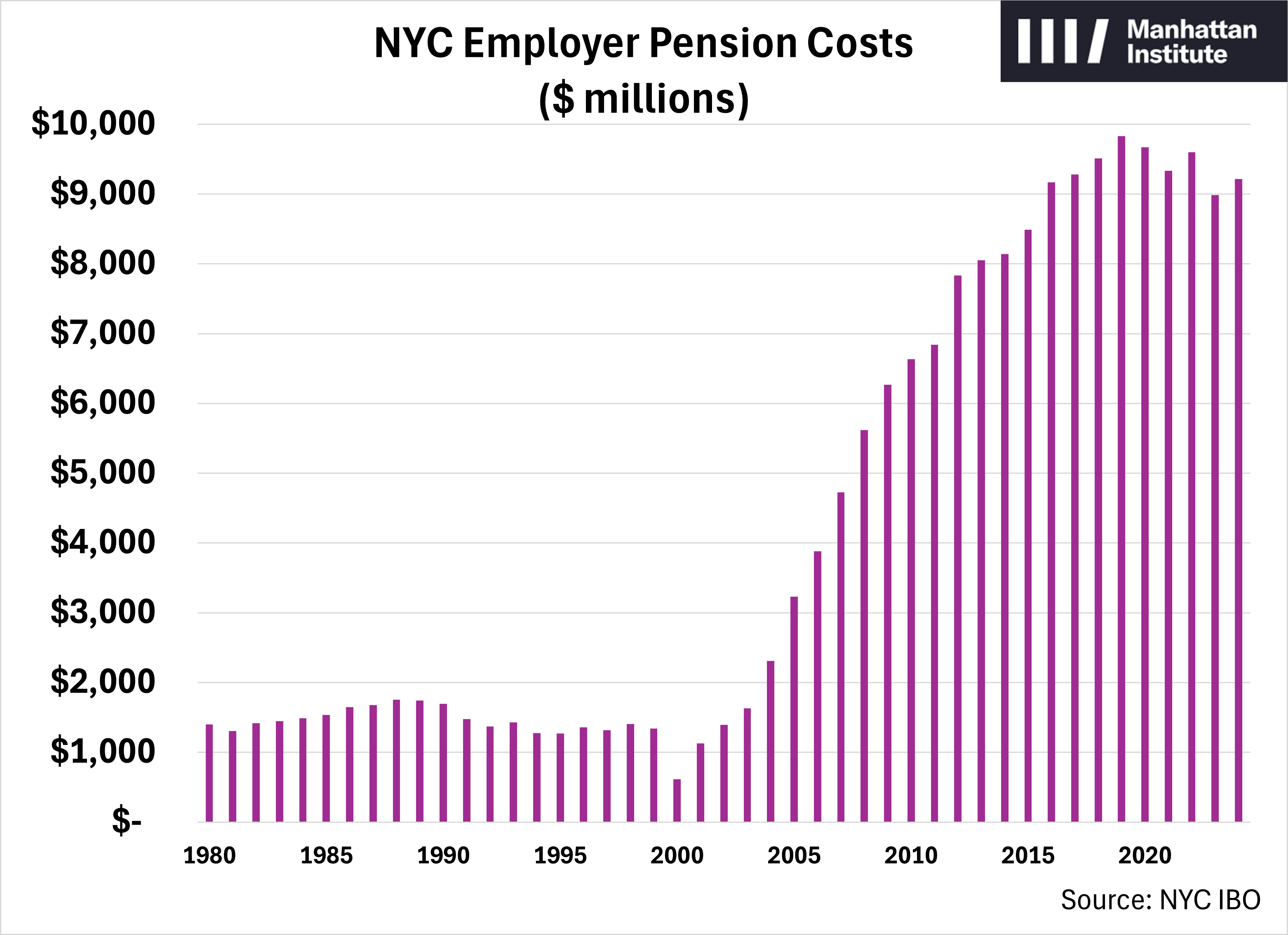

In the late 1990s, the city’s annual pension bill had been about $1.4 billion. The combined effects of underperforming investments and supersized benefits left taxpayers on the hook for massive sums. By 2009, the city’s pension costs had surged past $6 billion.

Put simply, by 2000, the Legislature had forgotten the lessons of the 1970s, and taxpayers paid the price.

In response, Albany passed two rounds of reforms, in 2009 under Governor David Paterson and in 2012 under Governor Andrew Cuomo. These changes, affecting only future hires, slowed the growth of pension costs.

The new standard retirement age for most people hired since 2012, into what’s called “Tier 6,” is 63 instead of 62 (police, fire, and other uniform employees have different rules).

They can no longer take early retirement at 55 with full benefits; they can start collecting at that age, but their pension is reduced. And they must contribute between 3 and 6 percent of their salary toward their own pension. A teacher making $100,000 per year pays about $6,000.

The reforms left New York public employees with what remains one of the most generous retirement packages still operating anywhere in the United States.

For the public employee unions, that’s not enough.

What “Fix Tier 6” Means

The United Federation of Teachers and District Council 37 — the city’s two largest unions, representing teachers and municipal workers — are feverishly pushing Albany to roll back the 2009 and 2012 reforms.

The unions argue, without evidence, that the changes seriously hurt the city’s ability to recruit and retain workers. This claim gained traction during the post-pandemic labor shortage, when every employer — public and private — struggled to fill positions, and the unions have been making the most of that argument ever since. Never mind the fact that the size of the public workforce has rebounded. New York state agencies have more employees today than at any time since 2018, and with the rising availability of automation, they should be getting smaller.

The unions say they’re demanding “tier parity,” bemoaning the very thought of people in Tier 6 working alongside people in Tier 4, despite the fact that Tier 4 members worked alongside Tier 1 members for a generation.

The arguments are pretextual: the unions believe they have the raw political power to get lawmakers to agree to their demands. Evidence of a public benefit has been unnecessary.

They successfully pressed Albany into trimming the vesting time for pensions back down from 10 years to five in 2022, and in 2024 got pols to change the formula for how those pensions will be calculated, basing them on a higher three-year pay average instead of five years.

That last modification alone is today costing the city about $200 million per year, and at least one pension plan noted in its latest annual report that this adjustment was the biggest contributor to rising pension costs last year. A seemingly tiny tweak will cost the city more than $400 million per year at the end of the 2030s.

For context, Mayor Mamdani’s latest budget forecast assumes pension costs will rise this year and next, peaking around $11.5 billion before coming back down as a rising share of employees pay toward their pensions—as the 2009 and 2012 pension reforms bend the curve and control costs. Ironically, much of his new spending agenda relies on the city realizing savings made possible primarily by Cuomo, his former electoral foe.

The unions haven’t yet filed legislation gutting the pension reforms outright, and that is not an oversight. State law requires an official actuarial cost estimate before pension legislation can advance.

That number would be large enough to kill such a bill the moment it became public. But that’s all the more reason to conceal it. Once it becomes law, there’s nothing lawmakers, let alone taxpayers, can do to reverse it.

New Yorkers, statewide, would owe no less than an extra $100 billion over the next three decades. Only the plan actuaries know for sure, since the exact liability depends on the age and experience of hundreds of thousands of public employees. The plans would be responsible for paying their pensions sooner, and they would immediately start collecting less money. Taxpayers would make up the difference.

Put another way, every New York family would be on the hook for $20,000 in pension costs.

The unions hope to slip the changes into the state budget, which is negotiated behind closed doors among a small group of leaders and routinely passed using a procedural move that waives the normal public waiting period.

One thing is certain: New York City, as the state’s largest public employer, would absorb the biggest share of the cost increase. Mayor Bloomberg in 2012 estimated Albany’s second round of reforms alone would save city taxpayers $21 billion over 30 years—and that was based on what were then considerably more optimistic assumptions about how pension investments would perform.

If the city suddenly faces tens of billions of dollars in new pension costs, the bond rating agencies, which determine how cheaply the city can borrow money, will notice. A downgrade means every dollar the city borrows gets more expensive. Moody’s, even before any pension rollback has materialized, has already changed New York City’s outlook to negative.

Where Things Stand Right Now

Governor Kathy Hochul (and a handful of the Legislature’s Republicans) attended a “Fix Tier 6” rally in Albany this month. She boasted about previous tweaks instead of committing to future changes.

Both chambers of the state Legislature included references to pension sweeteners in their budget proposals, but no cost estimates. The mayor has been supportive of “fixing” the pension system, but like most other people lending support to the unions’ scheme, doesn’t seem to have been told how much that would actually cost.

The state budget deadline is April 1st.

If this passes, the mayor will wake up to discover the city’s pension liabilities have ballooned overnight, and that the city owes billions it hadn’t planned for. A large cohort of city employees, many with six-figure pay, would instantly stop paying anything toward their pensions. The priorities his administration has staked out will compete for resources against a pension bill that cannot, ever, be renegotiated downward.

The unions have decided that a teacher or office worker making $100,000 a year, contributing $6,000 toward a constitutionally guaranteed, inflation-protected, lifetime pension, is an injustice worth blowing up the city’s finances to correct.

Albany, right now, seems inclined to agree. The bill will go to you.

|

|